A couple of years ago I got a task of writing a module for pricing gamma swaps. I found the task quite difficult, as all I got to base on was an Excel spreadsheet with formulas that were clearly wrong and the few sources on the Internet that I found lacked details. This post (and maybe the next) describes things I learned at that time. Please keep in mind that I am not a quant – just a software guy, so it’s possible I got some of this wrong, maybe all. If you think this is the case please enlighten me in the comments.

One technique for solving problems is to find a practice problem – something easier, but similar enough that going through the exercise gives confidence that the method is sound and serves as a stepping stone to the more difficult one. In case of gamma swaps that simpler problem is pricing of variance swaps.

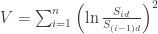

Variance swaps are financial instruments that are bets about the future observed variance of a price of an underlying asset. The parties that enter the contract observe the price

where

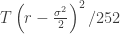

To answer this question suppose that the underlying price process is the geometric Brownian motion

Taking the expectation on both sides we get

(recall that

Now there is something I still don’t understand: in the pricing the first component is ignored – assumed equal to zero. Since typically

Anyway, whatever the rationale for ignoring that term is, as it was easy to guess the fair value of the variance swap strike is closely related to

(I)

This way by interpolating (and extrapolating as needed) the actual market values of

The rest of this post is about how to verify the identity above with Maxima Computer Algebra System (CAS).

(more…)