A couple of years ago I got a task of writing a module for pricing gamma swaps. I found the task quite difficult, as all I got to base on was an Excel spreadsheet with formulas that were clearly wrong and the few sources on the Internet that I found lacked details. This post (and maybe the next) describes things I learned at that time. Please keep in mind that I am not a quant – just a software guy, so it’s possible I got some of this wrong, maybe all. If you think this is the case please enlighten me in the comments.

One technique for solving problems is to find a practice problem – something easier, but similar enough that going through the exercise gives confidence that the method is sound and serves as a stepping stone to the more difficult one. In case of gamma swaps that simpler problem is pricing of variance swaps.

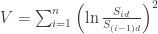

Variance swaps are financial instruments that are bets about the future observed variance of a price of an underlying asset. The parties that enter the contract observe the price

where

To answer this question suppose that the underlying price process is the geometric Brownian motion

Taking the expectation on both sides we get

(recall that

Now there is something I still don’t understand: in the pricing the first component is ignored – assumed equal to zero. Since typically

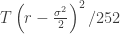

Anyway, whatever the rationale for ignoring that term is, as it was easy to guess the fair value of the variance swap strike is closely related to

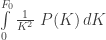

(I)

This way by interpolating (and extrapolating as needed) the actual market values of

The rest of this post is about how to verify the identity above with Maxima Computer Algebra System (CAS).

The first step is to define the Black-Scholes formulas for prices of Eropean call and put options:

assume(T>0,S>0,σ>0,r>0);

CN(x) := (1+erf(x/sqrt(2)))/2;

d1 : (log(S/K) + (r+σ^2/2)*T)/(σ*sqrt(T));

d2 : d1-σ*sqrt(T);

C : ratsimp(CN(d1)*S-CN(d2)*K*exp(-r*T));

P: ratsimp(CN(-d2)*K*exp(-r*T) - CN(-d1)*S);

Maxima can compute definite integrals, so it would be nice to just tell it to calculate the integrals in the (I) identity and be done. This fails however, apparently the task is beyond what Maxima can do. However, it is able to calculate the antiderivatives of

logexpand:super;

CiK2:expand(integrate(C/K^2, K))The result is too long to quote here in whole, but it is a sum of nine components:

C1:part(CiK2,1);

C2:part(CiK2,2);

C3:part(CiK2,3);

C4:part(CiK2,4);

C5:part(CiK2,5);

C6:part(CiK2,6);

C7:part(CiK2,7);

C8:part(CiK2,8);

C9:part(CiK2,9);

Those components are as follows (Maxima can export to LaTex, I just needed to replace \operatorname with \text ):

1:

2:

3:

4:

5:

6:

7:

8:

9:

Just in case, let’s check if Maxima is sure the sum of these expressions is the same as the original integral:

is(equal(CiK2,C1+C2+C3+C4+C5+C6+C7+C8+C9));Maxima responds “true”, so it must be. The formulas do not look tractable, but fear not. Let’s see how these terms behave as

C1L:limit(C1, K, inf);

C2L:limit(C2, K, inf);

C3L:limit(C3, K, inf);

C4L:limit(C4, K, inf);

C5L:limit(C5, K, inf);

C6L:limit(C6, K, inf);

C7L:limit(C7, K, inf);

C8L:limit(C8, K, inf);

C9L:limit(C9, K, inf);These nine limits turn out to be

1: 0

2:

3:

4:

5:

6:

7: 0

8:

9: 0

That does not look so bad, except for the limits 6 and 8 that are not finite. Fortunately the limit of the sum of the corresponding components is 0, so they cancel out at infinity:

C68L:limit(C6+C8, K, inf);

0The second limit can be simplified:

radcan(C2L);

So, we can compute the limit of the whole expression as

CIK2L:factor(C1L+radcan(C2L)+C3L+C4L+C5L+C68L+C7L+C9L);Which gives:

To get the integral from

F:S*exp(T*r);

CIK2F:subst(K=F,CiK2);

After adding some simplification code

CIK2Fs:expand(radcan(CIK2F));

factor_out(e1,e2):=if not is(op(e2)="+") then e2 else e1*apply("+",map(lambda([x],x/e1), args(e2)));

CIK2Fsf:factor_out(%e^(-T*r),CIK2Fs);

we get formula for CIK2Fsf to be

To check if the simplification code was ok we can do

is(equal(CIK2Fsf,CIK2Fs))

true

Now we can compute the integral from

CI:factor_out(%e^(-T*r),CIK2L-CIK2Fsf)

CIs:substpart(expand(part(CI,2)),CI,2);

and we obtain the call option integral of the identity as

Not nice, but not that horrible either.

Now it’s time to do the integral

PiK2:expand(integrate(P/K^2, K));

P1:part(PiK2,1);

P2:part(PiK2,2);

P3:part(PiK2,3);

P4:part(PiK2,4);

P5:part(PiK2,5);

P6:part(PiK2,6);

P7:part(PiK2,7);

P8:part(PiK2,8);

P9:part(PiK2,9);Let’s check if we have all the components of the sum:

is(equal(PiK2,P1+P2+P3+P4+P5+P6+P7+P8+P9));

trueNow let’s compute the limits of the components at 0.

P1L:limit(P1, K, 0,plus);

P2L:limit(P2, K, 0,plus);

P3L:limit(P3, K, 0,plus);

P4L:limit(P4, K, 0,plus);

P5L:limit(P5, K, 0,plus);

P6L:limit(P6, K, 0,plus);

P7L:limit(P7, K, 0,plus);

P8L:limit(P8, K, 0,plus);

P9L:limit(P9, K, 0,plus);

This gives us the following limits:

1:

2:

3:

4:

5:

6:

7: 0

8:

9:

Again we try to group the problematic limits so that we get finite values. First, we can show that limit of P6+P8 at 0 is 0:

P68L:limit(factor(P6+P8),K,0,plus);

0The limit of P1+P9 is a bit more difficult.

fP1P9:factor(P1+P9);This gives us that P1+P9 is

Now denote the

X:part(fP1P9,1,1,2,1);

is(equal(factor(P1+P9),-S*(X-1)/(2*K)));

trueTurns out, the right limit of X at 0 is 1:

limit(X, K, 0, plus);

1Hence we can apply L’Hôpital’s rule to calculate the limit of P1+P9 at 0:

P19L:-S*limit(diff(X-1,K),K,0,plus)/2;

which turns out to be 0.

Finally we have the following for the limit of the put integral at 0:

PIK2L:factor_out(%e^(-T*r),P19L+P2L+P3L+P4L+P5L+P68L+P7L);which gives

The antiderivative PiK2 of

PIK2F:subst(K=F,PiK2);

PIK2Fs:expand(radcan(PIK2F));

So the definite integral corresponding to put options in the identity (I) is

PI:factor_out(%e^(-T*r),PIK2Fs-PIK2L);

We add that to the formula for the call part obtained above and the miracle happens:

VS:radcan(PI+CI);

QED

Tags: Maxima, Variance swaps

Leave a comment